Personal injury protection (PIP) is defined as a type of auto insurance that pays for your medical bills, lost wages, and related expenses after a car accident, regardless of who caused it. Formally known as no-fault insurance, PIP activates through your own insurer without waiting for a fault determination. Twelve states mandate PIP coverage as of 2026, including Florida, Michigan, and New York. PIP coverage extends beyond emergency care to include rehabilitation, childcare, and funeral costs. Understanding what is personal injury protection can mean the difference between financial stability and serious debt after a crash.

What does personal injury protection cover?

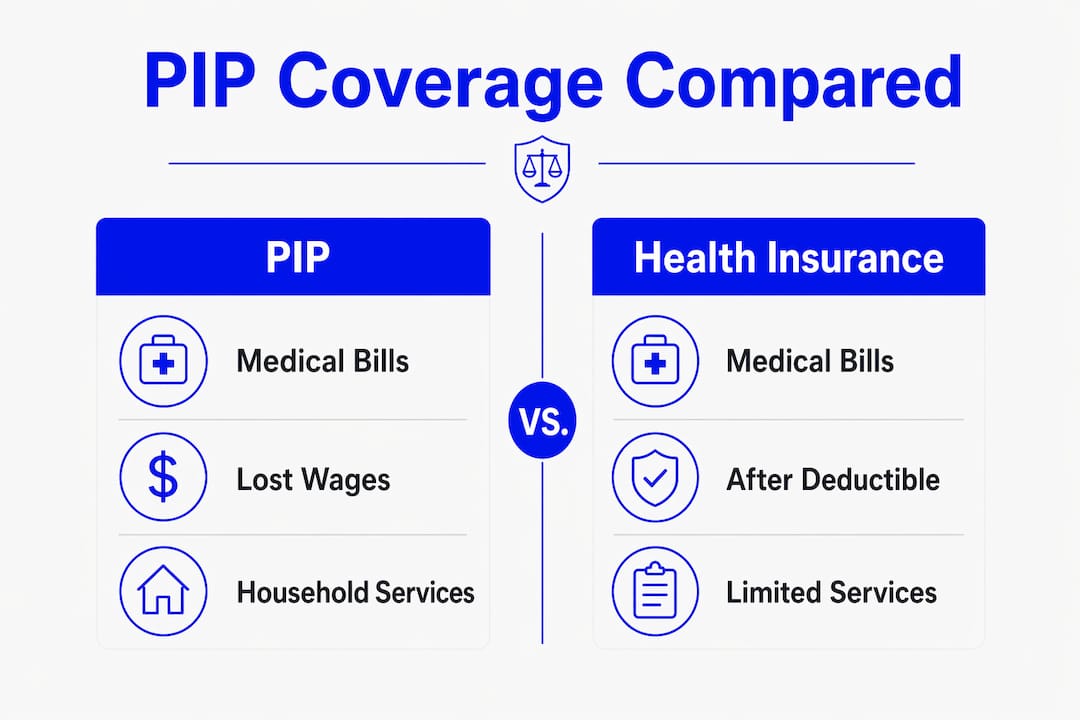

PIP covers a wider range of expenses than most drivers expect. Coverage includes medical bills, rehabilitation, lost wages, childcare, essential services, and funeral and survivor benefits. That breadth makes PIP one of the most practical coverages in a standard auto policy.

The mechanics are straightforward. After an accident, you file a claim with your own insurer. PIP pays before health insurance in no-fault states, covering deductibles and copays that would otherwise come out of your pocket. That sequencing protects your health insurance benefit limits and reduces your total out-of-pocket exposure.

PIP also covers costs that health insurance never touches. Childcare, house cleaning, yard work, and other services you cannot perform while recovering are all eligible expenses. If you are laid up for six weeks after a rear-end collision, PIP can pay someone to watch your kids and mow your lawn.

Pro Tip: Ask your insurer to clarify whether your PIP policy covers passengers and pedestrians, not just the named driver. Many policies extend to anyone in your vehicle at the time of the accident.

The table below shows how PIP compares to health insurance and MedPay across key coverage categories.

| Coverage category | PIP | Health insurance | MedPay |

|---|---|---|---|

| Medical bills | Yes | Yes (after deductible) | Yes |

| Lost wages | Yes | No | No |

| Rehabilitation costs | Yes | Partial | No |

| Childcare and household services | Yes | No | No |

| Funeral and survivor benefits | Yes | No | No |

| Fault requirement | None | None | None |

Which states require personal injury protection?

PIP is mandatory in 12 states as of 2026. Those states are Florida, Hawaii, Kansas, Kentucky, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Dakota, Pennsylvania, and Utah. Each state insurance commissioner sets minimum coverage limits, and those minimums vary widely.

In mandatory states, PIP functions as the primary payer before any other coverage kicks in. Michigan operates the most complex no-fault system in the country, offering unlimited medical coverage as a base option alongside lower-cost tiers. New York requires a minimum of $50,000 in PIP coverage per person. Florida requires $10,000, which many accident attorneys consider insufficient for serious injuries.

Outside these 12 states, PIP is optional. Drivers in optional states often skip it, assuming health insurance fills the gap. That assumption is costly. Health insurance does not replace lost wages, and high-deductible plans leave significant medical expenses uncovered in the weeks after an accident.

The states where PIP is mandatory include:

- Florida

- Hawaii

- Kansas

- Kentucky

- Massachusetts

- Michigan

- Minnesota

- New Jersey

- New York

- North Dakota

- Pennsylvania

- Utah

Drivers in optional states should treat PIP as a financial safety net, not a luxury add-on. Self-employed individuals and anyone without short-term disability coverage face the greatest income risk after an accident.

What are the financial benefits and limits of PIP?

PIP replaces a meaningful portion of your income when you cannot work. PIP policies typically replace 60%–80% of lost income, with some insurers paying up to 85%. Health insurance replaces none of it. That gap is the single most underestimated financial risk after a car accident.

Rehabilitation costs for physical and occupational therapy often exceed initial emergency room bills over the full recovery period. A broken leg may cost $8,000 in the ER but $20,000 in follow-up physical therapy. PIP covers both, up to your policy limit.

The cost of carrying PIP is low relative to the protection it provides. A $10,000 PIP policy costs approximately $20–$40 per month. Drivers relying only on high-deductible health plans face average out-of-pocket expenses of $3,000–$5,000 after serious accidents without PIP. That single statistic makes the math clear.

Pro Tip: If you are self-employed or your household depends on your income, select PIP limits above the state minimum. The monthly premium difference between $10,000 and $50,000 in coverage is often less than $20.

| Coverage type | Lost wage replacement | Rehabilitation | Household services |

|---|---|---|---|

| PIP (typical) | 60%–85% of income | Yes, up to policy limit | Yes |

| Health insurance | 0% | Partial | No |

| MedPay | 0% | No | No |

PIP does have limits. Once you exhaust your policy limit, you bear the remaining costs. Serious accidents involving long-term disability can exceed even generous PIP limits. That is when legal representation becomes critical to recovering full compensation.

How does PIP differ from other auto insurance coverages?

PIP, MedPay, bodily injury liability, and health insurance each serve a distinct purpose. Confusing them leads to coverage gaps that cost real money.

PIP covers your own injuries regardless of fault. Bodily injury liability covers other parties if you are at fault. These two coverages are not interchangeable. You need both if you want complete protection.

MedPay covers only medical costs, while PIP also covers lost wages and essential household services. MedPay is simpler and cheaper, but it leaves income replacement entirely uncovered. For a salaried employee with strong health insurance, MedPay may suffice. For anyone else, PIP is the stronger choice.

Key distinctions at a glance:

- PIP: Covers your injuries, lost wages, and household services regardless of fault. Pays before health insurance in no-fault states.

- Bodily injury liability: Covers injuries you cause to other people. Does not cover your own injuries.

- MedPay: Covers your medical bills only. No wage replacement, no household services.

- Health insurance: Covers medical treatment after your deductible. Does not cover lost wages, household services, or immediate copays before the deductible is met.

PIP is frequently called no-fault insurance because it pays without waiting for legal fault determination. That speed matters. When you need surgery or physical therapy, waiting months for a liability determination is not a viable option. PIP removes that wait entirely.

Key Takeaways

PIP is the most financially complete auto insurance coverage for accident victims because it replaces lost income, covers rehabilitation, and pays before health insurance, regardless of fault.

| Point | Details |

|---|---|

| PIP pays first | In no-fault states, PIP pays before health insurance, covering deductibles and copays immediately. |

| Income replacement | PIP replaces 60%–85% of lost wages, a gap health insurance and MedPay cannot fill. |

| 12 states mandate PIP | Florida, Michigan, New York, and 9 other states require PIP; optional states still benefit from it. |

| Low cost, high value | A $10,000 PIP policy costs $20–$40 per month and prevents thousands in out-of-pocket expenses. |

| Broader than medical bills | PIP covers childcare, household services, rehabilitation, and funeral costs beyond ER expenses. |

Why I think most drivers underestimate PIP

Most drivers I talk to assume their health insurance makes PIP redundant. That assumption is wrong, and it costs people money every year.

Health insurance does not pay your mortgage when you are out of work for two months. It does not hire a babysitter while you recover from a fractured pelvis. PIP does both. The income replacement feature alone justifies the monthly premium for anyone who lives paycheck to paycheck or runs their own business.

The other misconception is that PIP only matters if the accident is your fault. It does not matter at all whose fault it was. PIP pays from your own policy, immediately, while fault is still being sorted out. That speed is the real value. Medical providers want payment now, not after a six-month liability investigation.

I also see people skip PIP because their state does not require it. That logic is backwards. Optional coverage is still useful coverage. Even in states where PIP is not mandatory, it remains especially valuable for self-employed individuals or anyone without short-term disability insurance. The people who need it most are often the ones who opt out.

If you have a high-deductible health plan and no disability coverage, PIP is not optional in any practical sense. It is the only layer of financial protection that activates immediately after an accident and covers the full picture of your recovery costs.

— Gerard

When a PIP claim needs legal support

Understanding your personal injury coverage is the first step. Getting every dollar you are owed is the second.

PIP pays quickly, but it does not always pay enough. Serious accidents involving long-term rehabilitation, permanent injury, or disputed claims require legal expertise to resolve fully. Carcollisionlawyer connects accident victims with trusted attorneys who specialize in accident injury compensation and know how to maximize recovery beyond basic PIP limits. The free evaluation process at Carcollisionlawyer lets you understand your legal options without any upfront commitment. If your PIP limits have been exhausted or your claim has been disputed, speaking with an attorney is the right next step. Get your free injury claim review today and find out what you may be entitled to.

FAQ

What is personal injury protection in simple terms?

PIP is auto insurance that pays your medical bills, lost wages, and related expenses after a car accident, no matter who caused it. It activates through your own insurer without waiting for a fault determination.

Is personal injury protection the same as health insurance?

No. Health insurance covers medical treatment after your deductible but does not replace lost wages or pay for household services during recovery. PIP covers all three and pays before health insurance in no-fault states.

How much does PIP insurance cost?

A $10,000 PIP policy typically costs $20–$40 per month. Higher limits cost more but provide significantly greater protection against income loss and extended rehabilitation costs.

Do I need PIP if my state does not require it?

PIP is worth carrying even in optional states, particularly if you are self-employed, lack short-term disability coverage, or carry a high-deductible health plan. It fills income and service gaps that no other coverage addresses.

What is the difference between PIP and MedPay?

MedPay covers only medical bills. PIP covers medical bills plus lost wages, rehabilitation, childcare, household services, and funeral costs. For most drivers, PIP provides meaningfully broader protection at a modest additional cost.