Car accident lost wages recovery is the process of claiming the income and benefits you lose when injuries from a crash prevent you from working. This covers more than your base salary. Bonuses, commissions, overtime, sick days used, and employer-paid benefits all qualify. Accurate documentation and a clear understanding of the car accident claim process determine how much you recover. This guide walks you through how to calculate your loss, gather the right evidence, file your claim, and avoid the mistakes that cost injured people money every year.

How to calculate lost wages after a car accident

The standard formula for lost wages compensation starts with your annual salary divided by 2,080 work hours, then multiplied by the number of hours you missed due to injury. The 2,080-hour divisor represents a standard full-time work year of 52 weeks at 40 hours per week. That figure gives you a precise hourly rate, which you then apply to every hour you could not work.

Most injured people stop there. That is a costly mistake. Missed overtime, bonuses, and commissions are valid parts of any lost wages claim and must be documented separately. If you regularly worked 10 hours of overtime per week before the crash, that income belongs in your calculation.

Employer-paid benefits add another layer that most claimants overlook entirely. Benefits often account for roughly 30% of total compensation. That means health insurance, retirement contributions, and paid leave your employer covered all have real dollar value. Leaving them out of your claim is leaving money on the table.

Here is a practical example. Say you earn $60,000 per year and missed 320 hours of work. Your hourly rate is $28.85. Multiply that by 320 hours and you get $9,232 in base lost wages. Add documented overtime and benefits, and your actual car accident income loss could easily exceed $12,000.

- Calculate your hourly rate: annual salary divided by 2,080.

- Multiply your hourly rate by total hours missed.

- Add lost overtime, commissions, and bonuses with supporting records.

- Calculate the dollar value of employer-paid benefits for the missed period.

- Total all figures to arrive at your full wage loss claim amount.

Pro Tip: Document every income stream before you file. Claimants who include overtime, bonuses, and benefits in their initial demand recover significantly more than those who only submit base salary figures.

What documents do you need for a lost wages claim?

Strong, clear documentation is the single most important factor in winning a lost wages claim. Insurers scrutinize evidence for inconsistencies, and vague or incomplete records give adjusters the justification they need to deny or reduce your payout.

Employer wage verification forms confirm your job title, pay rate, work schedule, and the specific days you missed. These forms carry significant weight because they come directly from your employer and are difficult to dispute. Request one as soon as you know you will miss work.

Tax returns add another layer of credibility. W-2 and 1040 forms are filed under penalty of perjury, which makes them highly authoritative income evidence in wage loss cases. Insurance adjusters and courts treat them as reliable proof of your earnings history.

The documents you need fall into three categories:

- Income records: Recent pay stubs (at least three months), W-2 forms, 1040 tax returns, commission statements, and bonus documentation.

- Medical records: Doctor's notes specifying your diagnosis, physical restrictions, and the exact dates you were unable to work. Vague notes like "patient should rest" are far weaker than notes that state "patient cannot perform standing work for six weeks."

- Employer records: Wage verification forms, attendance records, and written confirmation of any missed shifts, meetings, or scheduled overtime.

Pro Tip: Contact your employer and doctor within the first week after your accident. Early, specific documentation is far harder for an insurer to challenge than records gathered months later.

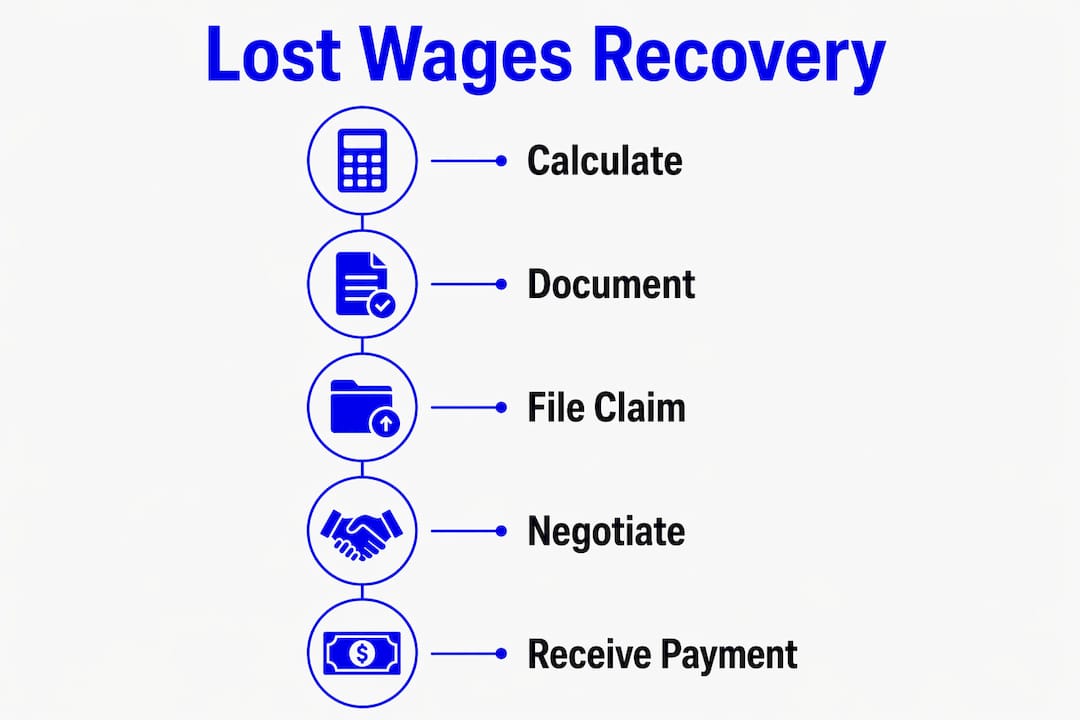

How does the car accident claim process work for lost wages?

The car accident claim process for lost wages differs based on whether you live in an at-fault or no-fault state. That distinction shapes your timeline, your strategy, and your potential recovery amount.

In at-fault states, you file a claim against the driver who caused the crash. Claims in at-fault states take longer because liability must be proven before any payment is made. The upside is that there is no automatic reduction in your recovery based on fault percentages, as long as you were not partially responsible.

In no-fault states, your own personal injury protection (PIP) insurance pays your wage loss benefits first, regardless of who caused the accident. PIP coverage has limits, and if your losses exceed those limits, you may need to pursue the at-fault driver's insurer for the remainder.

Here is how the claim process unfolds in practice:

- Notify your insurer within the required timeframe, typically within days of the accident.

- Gather all documentation including medical records, employer verification, pay stubs, and tax returns.

- Submit a demand letter to the at-fault driver's insurer. The letter should state your total wage loss, attach supporting documents, and specify the compensation you are requesting.

- Respond to adjuster requests promptly. Adjusters will verify your employment, contact your employer, and review your medical records.

- Negotiate the settlement. Insurers routinely offer less than the documented amount. Counter with your full calculation and supporting evidence.

- Accept a settlement or file suit. In at-fault states, a lump-sum settlement that includes lost wages typically requires waiting until medical treatment is complete and liability is clear.

Partial fault complicates recovery. If you were found 20% at fault in a comparative negligence state, your wage loss recovery is reduced by 20%. Document everything that supports your version of events to minimize any fault assigned to you.

Statutes of limitations impose hard filing deadlines, often around two years from the date of injury. Missing that deadline forfeits your right to any compensation, regardless of how strong your claim is.

| Claim type | Liability requirement | Typical timeline | Recovery potential |

|---|---|---|---|

| At-fault state claim | Must prove other driver's fault | Longer, tied to liability | Higher, no automatic reduction |

| No-fault PIP claim | No fault required | Faster initial payment | Capped by policy limits |

| Partial fault claim | Shared liability assessed | Varies by state rules | Reduced by your fault percentage |

Common mistakes that reduce your wage loss compensation

The most damaging mistake injured people make is failing to include all income components in their claim. Non-salary benefits are commonly overlooked but can increase recoveries by nearly a third. Submitting only your base salary figure leaves a significant portion of your legitimate loss unclaimed.

Gaps in medical documentation are the second most common problem. Insurers require a direct, documented link between your injury, your physical restrictions, and your specific missed workdays. A doctor's note that does not mention work restrictions gives the adjuster room to argue that your absence was not medically necessary.

Failing to mitigate your losses is a legal obligation, not just a strategy. You must accept reasonable light-duty work if your employer offers it and your doctor approves it. Refusing light-duty assignments without medical justification can reduce your wage loss compensation significantly.

Other common pitfalls include:

- Inconsistent records: Payroll records that do not match your tax returns raise red flags with adjusters and can trigger a full audit of your claim.

- Delayed medical treatment: Gaps between your accident and your first doctor visit give insurers grounds to argue your injuries were not serious or were caused by something else.

- Missing deadlines: Every state sets its own statute of limitations. Missing the filing window ends your claim permanently.

- Accepting the first offer: Initial settlement offers from insurers are almost always lower than the documented loss. Counter with your full calculation.

Pro Tip: If an adjuster contacts you directly, you are not required to give a recorded statement without legal counsel. Anything you say can be used to reduce your claim. Consult an attorney before agreeing to any recorded interview.

Key Takeaways

Recovering lost wages after a car accident requires accurate calculation, thorough documentation, and timely filing within your state's statute of limitations.

| Point | Details |

|---|---|

| Use the standard formula | Divide annual salary by 2,080, multiply by hours missed, then add overtime and benefits. |

| Include all income components | Bonuses, commissions, and employer-paid benefits can add nearly 30% to your total claim. |

| Get employer verification early | Wage verification forms confirm pay rate and missed days and are difficult for insurers to dispute. |

| Know your state's rules | At-fault states require proving liability; no-fault states use PIP coverage with policy caps. |

| File before the deadline | Statutes of limitations, often around two years, are hard cutoffs with no exceptions. |

What I have learned from watching injured people fight for their wages

The injured people who recover the most are not the ones with the worst injuries. They are the ones who treated their claim like a paper trail from day one. I have seen clients with serious injuries walk away with reduced settlements because their doctor wrote "rest as needed" instead of "patient cannot perform any work duties for eight weeks." That one phrase cost them thousands.

The second thing that surprises people is how much the benefits calculation matters. Most injured workers think about their paycheck and nothing else. When you factor in health insurance, retirement contributions, and paid leave, the real cost of missing work is substantially higher than your take-home pay suggests. Insurers know this. They count on you not knowing it.

State law creates more variation than most people expect. The same injury, the same missed workdays, and the same documentation can produce very different outcomes depending on whether you are in a no-fault state with PIP limits or an at-fault state where you can pursue the full loss. Understanding which rules apply to you before you file changes your entire approach.

My strongest advice is this: get an attorney involved before you submit your demand letter, not after the insurer rejects it. Attorneys who handle personal injury claims regularly know exactly what adjusters look for and how to structure a claim that is hard to undervalue. The free evaluation offered by services like Carcollisionlawyer costs you nothing and can tell you immediately whether your claim has been undervalued.

— Gerard

How Carcollisionlawyer can help you recover what you are owed

Recovering lost wages after a crash is a detailed, document-heavy process. One missing form or a vague medical note can cost you thousands.

Carcollisionlawyer connects injured people with experienced attorneys who handle wage loss claims from calculation through settlement. The free evaluation process lets you understand your full entitlement before committing to anything. Attorneys in the network know how to document every income component, counter adjuster tactics, and file within your state's deadline. If you are unsure whether your current claim captures your full loss, a free case review through Carcollisionlawyer is the fastest way to find out. Start your free claim evaluation today.

FAQ

What counts as lost wages in a car accident claim?

Lost wages include your base salary, overtime, bonuses, commissions, sick or vacation days you used, and the dollar value of employer-paid benefits like health insurance and retirement contributions. Any income you would have earned but could not because of your injuries qualifies.

How do I prove lost wages to an insurance company?

You need an employer wage verification form, recent pay stubs, W-2 or 1040 tax returns, and medical records that specifically link your injury to your missed workdays. Vague documentation is the leading reason insurers reduce or deny wage loss claims.

How long do I have to file a lost wages claim after a car accident?

Statutes of limitations typically give you around two years from the date of your injury to file a personal injury claim, though the exact deadline varies by state. Missing this deadline permanently forfeits your right to compensation.

Does partial fault affect my lost wages recovery?

Yes. In comparative negligence states, your recovery is reduced by your percentage of fault. If you were 25% at fault, you recover 75% of your documented wage loss. Thorough evidence supporting your version of events minimizes the fault assigned to you.

Should I accept the first settlement offer for lost wages?

No. Initial offers from insurance companies are almost always lower than your fully documented loss. Counter with your complete wage calculation, including benefits and supplemental income, supported by employer verification and medical records.